Achieving a net worth of one million dollars is a significant accomplishment that can offer financial security and peace of mind. However, it’s crucial to avoid making common financial mistakes that can jeopardize your wealth and hinder your long-term financial goals. Here are three financial mistakes to avoid with your first million dollars:

Overspending and Lifestyle Inflation

One of the most common mistakes people make when they come into money is overspending and inflating their lifestyle. When you suddenly have access to more money, it’s easy to get carried away with extravagant purchases and lavish experiences. However, overspending can quickly deplete your wealth, leaving you with little to invest or save for the future.

Instead, it’s essential to maintain your spending habits and avoid lifestyle inflation. This means living within your means and not increasing your expenses significantly, even though you now have more money. Focus on saving and investing your money for the long term instead of spending it on short-term pleasures.

Failing to Diversify Your Investments

Another mistake to avoid with your first million dollars is failing to diversify your investments. Putting all your eggs in one basket, such as investing solely in real estate or the stock market, can be risky, as it exposes you to significant losses if that investment performs poorly. It’s crucial to diversify your investments across different asset classes, such as stocks, bonds, and real estate.

By diversifying your investments, you can reduce your overall risk and maximize your returns. However, it’s important to remember that diversification doesn’t guarantee a profit or protect against losses. It’s essential to conduct thorough research and consult with a financial advisor to determine the best investment strategies for your financial goals and risk tolerance.

Not Planning for the Future

Just because you’ve hit your first million doesn’t mean you can stop planning for the future. In fact, it’s more important than ever to plan for the long-term. This includes setting goals for retirement, estate planning, and creating a legacy for your family.

To ensure that your wealth is protected and your future is secure, consider working with a financial advisor. They can help you create a comprehensive plan that takes into account your current financial situation and your long-term goals.

In conclusion, hitting your first million is an incredible achievement, but it’s important to avoid these common mistakes to ensure long-term financial success. By avoiding overspending, diversifying your investments, and planning for the future, you can continue to build wealth and secure your financial future.

As you might have heard in the news, last Friday, March 10, 2023, Silicon Valley Bank (SVB) has collapsed and was ordered by regulators to shut down its business. Part of the reasons that its collapse caused great concern is that it is the biggest bank failure since the 2008 Financial Crisis.

The failure of SVB is caused by a classic bank run. SVB had cash deposits of many startup companies. As bad news about SVB started spreading, a large number of these companies along with other depositors scrambled to pull their money out of the bank at the same time. This created a bank run that doomed SVB.

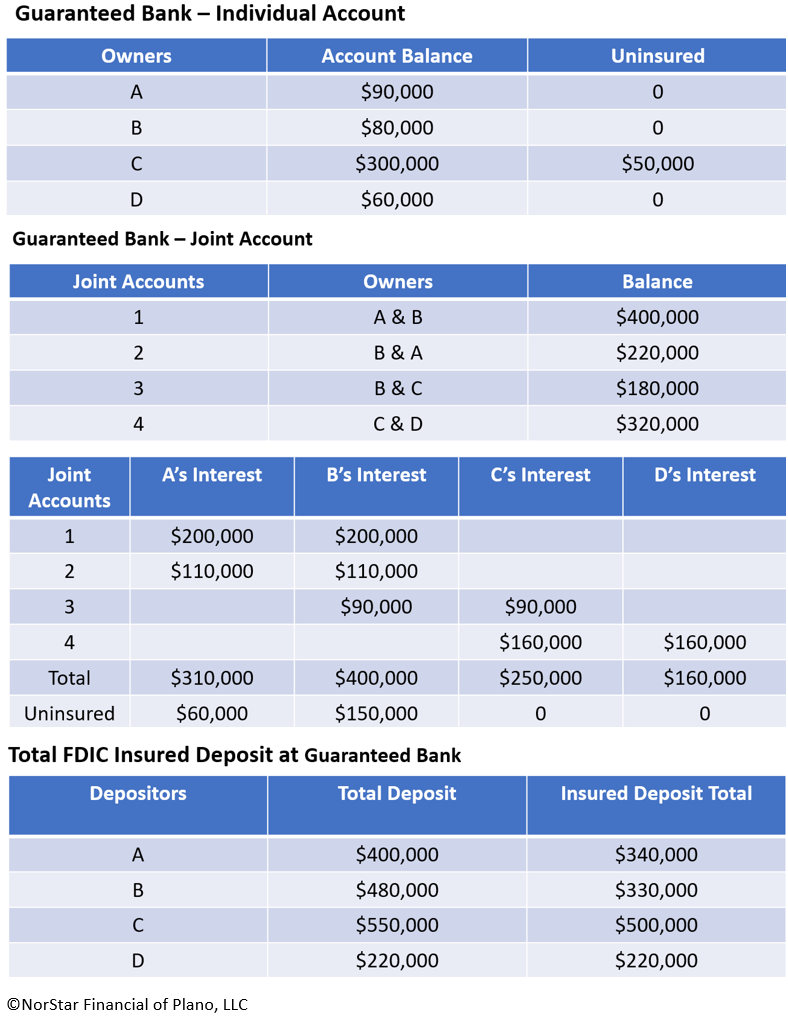

Naturally, you may wonder is my money safe in my bank?The Federal Deposit Insurance Corporation (FDIC) insures depositor accounts in banks and most types of nonbank thrift institutions up to $250,000. Deposits maintained in different categories of legal ownership, i.e. individual, joint account, irrevocable trust, and testamentary account are separately insured. As a result, a depositor can have more than $250,000 insurance coverage in a single institution. Here is how it works:

Likewise, the FDIC insures your deposits in each different institution in the same fashion as illustrated above. So, if you have $250,000 of deposit at each of four different banks, the FDIC insures a total of $1,000,000 of your deposits. As you can see, if you have a large sum of deposit exceeding $250,000, you need to either deposit the money into different types of accounts at the same bank, or spread the deposit among several banks.

Recently, Fidelity announced that it is launching a Fidelity Youth Account for 13 to 17 years old. The no-fee account allows teenagers to buy and sell stocks, exchange traded funds and Fidelity mutual funds. Fidelity pitches this new business as an education opportunity for teens to learn how to manage their money. So, should we cheer for the news that the brokerage house now allows teens to trade stocks? Not so fast.

First, since the start of pandemic last year, many of the new retail investors who entered the stock market are younger investors. Of the 4.1 million new accounts that Fidelity added in the first quarter of 2021, 1.6 million were opened by retail investors 35 and younger, an increase of more than 222% from a year prior, according to CNBC. Now, by allowing teens to trade stocks, is this another tactic for brokerage houses to attract money of even younger demographics?

Second, the name no-fee account is misleading. This could give teens the impression that trading is free. It could also encourage some investors to trade more. Numerous studies in the past have shown that frequent trading by timing the markets are detrimental to average investors’ long-term investment success.

Third, I am all for educating teens on sensible personal finance, but I think this time, it does the opposite of fostering good financial habit. According to a recent industry report that most of the Generation Z investors, people who were born between 1997 and 2015, get their investment advice from social media such as TikTok. Want to know what this means for investment world? Look no further than GameStop stock bubble earlier this year. This kind of investing habits are not unique to Gen Z investors. Think about how many of us who make investment decisions based on the “advice” or “tips” gotten from friends, coworkers, and/or online social media groups.

All in all, what I see from Fidelity’s latest venture is not a boon for teens and their families. If we really want to educate our teens on personal finance, teaching them the good habits of saving and budgeting, and understanding the impacts of personal debt are much more important than knowing how to trade stocks at this age.

Since the pandemic began early last year, there were increasing numbers of Americans who adopted so called “pandemic puppies”. These fur babies brought joys and companionship to many families who were confined to their homes due to governments’ lock down orders. Sadly, in a recent article USA Today reported that those dogs are being returned to shelters all cross the country.

I do not know all the reasons behind the surging numbers of returns of these dogs. But, I venture to say that if you have adopted puppies during the pandemic, with a little planning on your part things can work out pretty nicely between your puppies and you. The things you need to consider now that life has been gradually returning to pre-pandemic ways are how your new routines affect your dog and what the long-term costs of having a dog are. I will offer some tips on the financial part while leave it to you to figure out how to make your new routines work out for you and your dog.

Depending on the breed of the dog, some dog could incur a large amount of medical bills down the road. One way to mitigate the financial burden is to buy pet insurance. Do a cost/benefit analysis. Does it make sense to buy pet health insurance in your individual situation? Many pet insurances only cover cats and dogs, but a couple of insurers will also cover birds and reptiles. Before you purchase health insurance for your dog, be sure you understand what covered and excluded conditions are and how you file an insurance claim. Some plans do not cover routine office visits. Many pet insurance companies put their sample insurance policies on their websites. Locate these policies and read them carefully.

Our pets bring us joys and companionship, but they

also depend on us for continuous care. How to provide such care in case we are

not able to? The pandemic taught us how important it is for us to have some

kind of estate plan in place. Fortunately, pet trust can be a valuable tool for

pet owners to do so. So far, all 50 states of the U.S have passed laws allowing

pet owners to set up trusts for their companion pets. While considering setting

up a trust for your dog, it is a good practice to designate different parties

as caregiver of your dog and trustee that administers the funds in the trust

for your four-legged companion respectively.

Alternatively, pet owners can opt for a pet

protection agreement, which is simpler than setting up pet trusts, to protect

their pet. With a pet protection agreement, pet owners can name their pets’

guardians, leaving funds, and providing instructions for how to care for your

pets when you are not around.

Hopefully, with a bit of creativity and some

planning by you, the “pandemic puppy” will be your companion for many, many

years to come.

I call the period that runs from every September to next May college application season for high school seniors across the country. The 2020/21 college application season is almost over. Now it is time for most high school seniors to weigh the offers and envision the lives they will be living for the next four years.

This is a time of excitement as well as anxieties for both students and their families. As parents of soon-to-be college freshmen, they all want their children to have four successful college years. But, I know that “success” is a highly subjective word. And student’s college experiences may be different due to the kind of colleges or universities they attend.

So, first let us define what

success in college means. Success in college, according to many college

students themselves, means achieving good grades, graduating on time, maintaining

a balanced social life and landing a good job after graduation. On the surface,

these goals seem to be simple and easy to achieve, right? In reality, however,

there is no small number of students either struggle academically or have a

hard time fitting in socially.

After perusing books and articles

related to this subject and talking to some parents whose kids have already

gone through colleges, I found out some universal traits of college students

who have had positive experiences during college.

The first trait of such a student

is having definite goals for life. I cannot stress enough of the importance for

a college student to have definite goals for his or her life. But, there is a

caveat. The goals should be what the students truly want for themselves, not

the goals their parents or society set for them. Lucky are those who have

concrete goals even before they set foot on college campuses. These students

are motivated, self-driven and confident. They will seek and even create the

kind of college experiences that help them achieve these goals.

The second trait of a successful college student is having a good amount of self-control. The majority of high school seniors will leave their childhood homes and live in some kind of campus housing arrangements for the first time. No longer in their lives will there be nagging about eating healthy food and finishing their homework on time. At the same time, they are constantly facing the tasks of making choices: going to parties or working on that course assignment which is due very soon, eating healthy meals or eating whatever they want, and etc. Life is about trade offs. College life is no exception. The students who have successful college lives are those who are able to make good decisions most of the time. Generally speaking, making good decisions need good amounts of self-control.

The third trait of a successful college student is the possession of good study skills. Academics are a big part of college life. It is hard to believe that a college student is having a positive experience when he or she struggles academically. For students who lack confidence in this skill set, I would like to share with them the formula for academic success outlined in Purdue University’s Guide to Creating a Successful College Experience:

Read the syllabus

Go to every class

Sit near the frontin class

Find a study partneror group in every class

Take good notes.

At the beginning of each semester, ask yourself:

Do I understand what is expected of me in each class?

Do I have contact information for someone in every class to study with or contact in case I’m sick?

Manage your time wisely

Never let a week go by where you don’t understand the content in your courses

If you are confused or lost in a class, visit your professor, go to a help lab or study with a friend. Use your campus resources — they are there to help you

Study 2 hours for every hour you are in class

The fourth trait of a successful

college student is getting involved in a wide range of activities. We know that

college success is more than just good grades. Activities outside classrooms not

only enrich students’ lives, they also help students explore their interests,

develop social skills and possibly gain life-long friendships. Some of the

activities include volunteering, working part-time on campus, getting involved

in student’s residence hall, doing internships or studying abroad.

In addition to the above four traits, another factor affecting students’ college experiences is the emotional support or lack of it from their families. College years are coincident with a person’s transition period to adulthood. And this transition period is filled with stresses and struggles. In Janet Hibbs and Anthony Rostain’s apt named book – “The Stressed Years of Their Lives”, they talked about the mental problems facing today’s college students. Alarmingly, almost one-third of all college students report having felt so depressed that they had trouble functioning in the last twelve months according to the authors. Although so called “helicopter parents” are mocked and discouraged, this does not mean that parents can stay out of their college-age children’s lives other than writing tuition checks.

Before parents send off their children to college, they need to be aware of two important laws that could be critical to their children’s well beings. They are HIPAA and FERPA. HIPAA stands for Health Insurance Portability and Accountability Act. HIPAA protects a person’s confidential health information. FERPA stands for the Federal Educational Rights and Privacy Act of 1974. FERPA was designed to protect the privacy of educational records and to give students the right to inspect and review their educational records (collegiateparent.com).

In most states 18 is the legal age of majority, which means most college students’ health information and academic records are protected under law and not shared with their parents without the students’ consent. By checking the students’ academic records parents could detect early signs of their children’s mental issues. In order to access their students’ transcripts parents need a consent form to disclosure of FERPA protected academic records. In the age of Covid-19, it is also important for parents to have signed HIPAA waiver and health care proxy from their college-age children in order to make medical decisions on their children’s behalf. If parents need more information on these forms they can contact their financial advisors and/or family attorneys for help.

Looking back, 2020/21 college application process is quite a journey for both high school seniors and their families amid a global pandemic. As the high school seniors are about to open a new chapter of their lives, I wish them all successes in college.

ISO and NSO, what do these terms

mean? These terms stand for incentive stock options (ISOs) and non-qualified

stock options (NSOs or NQSOs) respectively. They are mostly common among

companies which use their company stocks as part of the employee’s compensation

and/or retirement benefit packages.

NSO or NQSO are options to buy shares

of company stock at a stated price and can be exercised over a specific period,

i.e. over 10 years. The exercise price is normally 100% of fair market value on

the date the option is granted, but it can be set lower.

ISO is an option to buy shares of

company stock at a set price on the date of grant and can be exercised over a

period of up to 10 years. Like NSO, the exercise price of ISO is normally set

at the fair market value on the date the option is granted.

After reading the above definitions

of ISO and NSO you are probably wondering: what are the differences of these

two options? The differences mostly lie in the employer tax deductions and income

tax treatment of exercising ISO and NSO options to the employees.

With most NSOs, if the employee opts to exercise the options to hold the shares of company stock, then the employee must recognize as ordinary income the amount of difference between the option grant (exercise) price and the fair market value of the underlying stock at the time of exercise. This income is subject to social security (FICA) and federal unemployment (FUTA) taxes. Subsequently, the employee will recognize either capital gains or losses on any appreciation or depreciation in the stock value from the day of exercise until the day the employee sells the stock. Alternatively, the employee can opt to exercise to sell, and then the employee will pay income and social security taxes on the amount realized on the sale of the stock minus the option price.

Unlike NSO, where the employee has to pay ordinary income taxes when he or she exercises the options to hold the stock, an employee who receives ISOs does not have to pay regular income tax at the time of exercise. If, after the exercise the shares are held for at least one year from the date of exercise and two years from the date of grant of the options (1year/2year holding period requirements), the sale of the shares will result in long-term capital gain from the date of the option grant to the date of sale of the stock. If, the 1year/2year holding periods are not met, then the sale becomes a disqualifying disposition and the ISO is treated like a NSO, where the difference between the option price and the fair market value at the time of exercise will be taxed as ordinary income.

The difference between the taxation

of a disqualifying disposition of an ISO and that of an NSO is that the

recognized ordinary income from the disqualifying ISO is not subject to social

security and federal unemployment taxes.

Here are two examples explaining

how ISO and NSO work:

Adam received 100 shares of NSOs from his employer ABC Industry, Inc. on February 8, 2017. The option exercise price is $5 per share. On the date of grant, there is no taxation to Adam. On March 15, 2018, when the fair market value of the ABC’s stock is $10 per share, Adam exercised his options. Adam would recognize $500 ($10-$5=$5 times 100 shares) as ordinary income. On March 20, 2019 when the ABC’s stock price rises to $20, Adam sells all of his 100 shares of ABC stock. Adam would recognize $1,000 as long-term capital gain and would pay capital gain taxes because he has held the stocks for more than 12 months after he exercise his NSOs. If, instead of exercising the NSOs on March 15, 2018, Adam waited until March 20, 2019 to exercise the option and simultaneously sell the underlying stock, then, Adam would recognize all proceeds from the sale, $20 stock price/share – $5 option price times 100 shares = $1,500, as ordinary income and would pay regular income tax and social security taxes on this $1,500.

Eve received 100 ISOs from XYZ Industry Inc. on January 28, 2017. The option exercise price is $5 per share. If Eve exercised her ISOs on January 31, 2018 when the fair market value of the stock was $10 per share, she would recognize no income for regular tax purposes. If subsequently, Eve sells the stocks when its price rises to $20 on February 9, 2019, she would be able to recognize the entire gain of $ 1,500 as long-term capital gain because she has met the 1year(from exercise)/2 year(from grant) holding period requirements. If, Eve sells the stocks on December 31, 2018, then she has not met the 1year/2year holding period requirements. In this case, the $500 from the exercise of the options on January 31, 2018 would be treated as ordinary income and the subsequent gain of $1,000 from sale of the stocks on December 31, 2018 would be recognized as short-term capital gains.

With NSO, the employer can take a

deduction in the amount of income that is taxed to the employee. With ISO,

however, if the employee complies with the 1year/2year holding period

requirements, the employer gets no tax deduction from it.

If an employee is given stock

options, he or she needs to be clear what kind of options they are. There is an

employment requirement for employees who receive ISOs. That is, the employee

who receives ISOs must remain employed with the same employer from the time of

the grant of the options until at least 3 months before the exercise.

Another difference between these

two employee stock options is that ISOs are not transferable except at death,

while NSOs are transferable during the employee’s lifetime.

2020 is finally behind us. What is your plan for year 2021? Here I outlined some financial tips for you to put on your early 2021 to-do list to jump start the year to be a successful and prosperous one for you and your loved ones. Below are some of the essential personal financial information you will want to save and keep in handy as your reference guide throughout the year.

Adjust your retirement plan contributions for 2021

2021 retirement plan contribution limits

Plan

Maximum Deferral

Age 50 and Over Catch-up Contribution

401(k)/403(b)

$19,500

$6,500

Deductible IRA

$6,000

$1,000

Non-Deductible IRA

$6,000

$1,000

Roth IRA

$6,000

$1,000

The individual IRA contribution deadline for 2020 is April 15, 2021.

Phase out range for deductible IRA is $105,000-$125,000 for joint filing if covered by a workplace retirement plan; Phase out range for Roth IRA is modified AGI from $198,000-208,000 for joint filers.

Health Savings Account Contribution Limit for 2021:

Self-only

Family Coverage

Contribution Limit

$3600

$7200

Contribution Limit over age 55

$4600

$8200

High-deductible health plan minimum deductible

$1400

$2800

High-deductible health plan out-of-pocket maximum

$7000

$14,000

Keep in mind these important income tax facts for 2021:

2021 Income Tax Brackets and Rates:

Tax Bracket

Single Filer Income Range

Married File Jointly Income Range

10%

$9,950 or less

$19,900 or less

12%

$9,951- $40,525

$19,901 – $81,050

22%

$40,526 and $86,375

$81,051 and $172,750

24%

$86,376 and $164,925

$172,751 and $329,850

32%

$164,926 and $209,425

$329,851 and $418,850

35%

$209,426 and $523,600

$418,851 and $628,300

37%

$523,601 or more

$628,301 or more

The standard deduction

is $12,550 for individuals and $25,100 for married couples filing jointly.

2021 Alternative Minimum Tax (AMT) Exemption Amounts:

Single or Head of Household

Married File Jointly or Qualified Widow

Married File Separately

Maximum Exemption

$ 73,600

$ 114,600

$ 57,300

25% reduction if over:

523,600

1,047,200

523,600

Exemption Eliminated

818,000

1,505,600

752,800

2021 Qualified Dividend and Long-term Capital Gain Tax Rate:

Income Range: Single filer

Income Range: Married file jointly

Capital Gain Tax Rate

$0-$40,400

$0-$80,800

0%

$40,401-$445,850

$80,801-$501,600

15%

Over $445,850

Over $501,600

20%

Net Investment Income Tax:

Individuals will owe the tax if they have Net Investment

Income and also have modified adjusted gross income over the following

thresholds:

Filing Status

Threshold Amount

Married filing jointly

$250,000

Married filing separately

$125,000

Head of household (with qualifying person)

$200,000

Qualifying widow(er) with dependent child

$250,000

Single

$200,000

The Net Investment

Income Tax (NIIT) applies at a rate of 3.8% to certain net investment income of

individuals, estates and trusts that have income above the statutory threshold

amounts.

Annual Exclusion for Estates and Gifts

In 2021, the first $15,000 of gifts to any person

is excluded from tax.

Since 2018, the Tax Cuts and Jobs Act temporarily increased the basic exclusion amount for estate and gift taxes for tax years 2018 through 2025, with both dollar amounts adjusted for inflation. For 2021 the exclusion amount is $11,700,000 per individual, and $23,400,000 for a couple.

Review your Insurance policies

If your situation has changed during 2020, such as change of job, birth of a new child, or purchases of new car, house, etc., you need to review your insurance coverage or talk to your financial adviser to help you come up with proper coverage amount for your current insurance needs.

Don’t forget the deadline for individual tax filing is Thursday

April 15, 2021.

Gather and organize all your

paperwork such as W-2 forms, bank statements, mortgage payment statements,

property tax receipt, business expenses, investment statements from your

broker-dealers, charity donation receipts, etc. for your 2020 tax filing.

A couple of events that you might want to keep an eye on:

House Ways and Means Committee Chairman Richard Neal plans to reintroduce in the new Congress the Securing a Strong Retirement Act of 2020, which would boost the required minimum distribution age from 72 to 75. In 2019, the Secure Act passed by congress has pushed the age that retirement plan participants need to take the required minimum distributions (RMD) from 701/2 to 72. If this new bill passes, it would create more favorable financial planning opportunities to people contributing to various retirement plans.

Another thing to watch for is for families with kids applying for college in the fall 2021. The dates and places of taking the SAT/ACT had been changed a couple of times last year by the institutions which offer these tests due to the pandemic. Since the pandemic is still going on parents need to make sure their high school kids know the exact dates and places of taking these tests. Parents and students can go to www.collegeboard.org to check out the latest updates on SAT test or www.act.org for ACT tests.

As I am reflecting back on year 2020 there is no doubt that coronavirus pandemic is the biggest theme of this year. The pandemic has not only disrupted global economy, it also changed our lives more or less. Last December when I wrote an article on looking into year 2020, “uncertainty” and “change” were the two words that came to my mind at that time. This time, I think “resilience” and “recovery” will be the two theme words of year 2021.

Resilience is the US economy which bounced back from its second quarter low on a tear. Resilience also is human spirit that carries us over despite lock-downs and remote working/learning. Now that we have clinically proven effective vaccines we see light at the end of this dark tunnel. We are entering the stage of recovery.

But we are still vulnerable coming out of this pandemic. Recent weeks’ numbers of US initial jobless claims were still stubbornly high, pointing to a slow-down and weak recovery well into the year 2021. Many economists pointed out that it is highly likely that we will not have a full economic recovery until after the end of year 2022.

It is hard to predict the short term trend of the stock market. Due to the pandemic caused economic downturn, the Fed and the government will continue to support the US economy with fiscal and monetary policies at least in the short term. These temporary stimulus policies in turn will most likely sustain the stock market’s high valuations in much of the year 2021.

We probably will not see drastic changes in tax law in 2021 if the Republicans win the Senate majority. However, several rounds of economic stimulus packages passed during the Pandemic widen the government deficits. Therefore, mid-term to long-term there could be quite significant changes to current tax law, especially rolling back of 2017 tax cuts for the rich and corporations.

When it comes to personal finance, there are a few strategies for you to plan for year 2021. That is, budget and track your spending; manage your debt and increase your emergency reserve.

If you have not had money set aside for rainy days, start building your rainy day reserve fund as soon as possible. Build the fund to cover at least three months of family expenses. If you already have three months of expenses of emergency fund set aside, preferably in savings account or money market fund, increase the reserve to cover six months of expenses. If personal financial situation allows it, it is better to increase the emergency reserve to cover 12 months of expenses at this time.

The reason I am recommending the increase in emergency reserve is because entering 2021 there are still many uncertainties, including possible continued pandemic, relatively high stock market volatility and weaker than expected economic recovery that may all affect your job and financial stability. It is wise to have a larger than usual monetary cushion to carry you over during these unprecedented times. And if the economy recovers much faster than we predicted, then you will need less emergency reserve and have some extra money to take advantage of the opportunities emerged in the financial market and elsewhere in the coming year.

Thanks for reading and have a very

happy holiday season!

In our June article we talked about

whether or not parents should allow their college aged children to have their

own credit cards. This time we will continue our teen and money topic. As

parents we want to raise financially responsible children. If our last article

is geared toward older teens, in this one we will show parents a good way to

allow their younger teens a real-life chance of managing their own money.

Have you thought about allowing your

teens to have their own bank accounts? Some banks offer kids or teen

checking/savings account designed for their young customers.

In our family, our two teenage daughters do some basic chores, not expecting getting paid. Purposefully, my husband and I asked them to do a few extra household chores in exchange for allowance money. They are getting paid twice a month. For this reason, my husband and I set higher standards of the quality of the job they do than the basic chores they are expected to do. At the same time, I opened teen savings account for them at a bank so that their “wage” goes to the bank accounts in their names. We also set up accounts for them at Mint.com, an online personal finance management website and linked their bank accounts with their Mint.com accounts.

Part of our strategies of teaching

them financial responsibility is to give our daughters great freedom to spend

their money however they want unless the purchases are explicitly banned by us.

In the past, when they go out with friends to places, like mall, they would ask

us for some money. Since having their own bank accounts, they don’t have to

argue how much money they need to bring with them anymore. They can just take

their bank debit cards with them and go.

As expected, during the first couple of months they managed their money poorly. They made a few big purchases and their bank accounts depleted quickly. Then, they have to wait for their next “pay” deposit even if they see something they really want to have. After a while they started to learn to budget and save for “big ticket” items. And they also learnt to postpone consumption so that they leave some money in the bank in case of “unexpected” needs. They are learning these essential personal finance management skills all by themselves without me or their dad to sit down and talk them into doing so.

One of the features of these teen

bank accounts is that parent can be a co-owner. This allows parents to monitor

and supervise while giving their teens freedom to manage their money. This

should assuage concerns of some wary parents who want some control on their

kids’ spending.

For interested parents, I will

compare some essential features of the checking accounts three banks offer for

their teen customers. If you do not bank with any of them, call your own bank

and ask them if they offer such accounts.

Bank of America

Capital One

Chase Bank

Teen Checking Account and Interest Rates

yes

Yes 0.1%APY

yes

Minimum to Open or Keep

Call to verify

$0

Call to verify

Monthly Fees

$0 if under 24

$0

$0 if under 18

Allow Parental Supervision

yes

yes

yes

Debit Card

yes

yes

yes

(Sources: official websites of BoA, Capital One Online Bank and Chase Bank)

The information in the table above gives you a glimpse of what the banking products for teens are out there. Don’t agonize about which one to choose, your goal is to let your teens learn to manage their money responsibly. Good luck!

Parents with college age children often face a dilemma: should we allow our kids to apply for a credit card of their own? If yes, what if they become irresponsible and rack up credit card debt? These are the legitimate concerns parents should have.

On one hand, young adults need to build their own credit history. With good, established credit history young adults could get favorable financial treatment when someday down the road they need to apply for loans to purchase a house or a car, or rent an apartment of their own. Therefore, it is beneficial for college students to have their own credit cards and build good credit scores by using them responsibly and pay the credit card companies in full and on time every month.

On the other hand, some of these students are still in their teen years, and the freedom of having a credit card to use is too tempting. It is not uncommon for college students to abuse credit cards and accumulate debts that they may hide from their parents, causing financial damages to themselves and their parents.

So, after stating the pros and cons of giving college students a credit card of their own, what can parents do?

This advisor thinks that there are several steps which parents can do to maximize the benefits of letting your college age kids have their own credit cards while minimize its potential financial harms.

As a parent, you need to start fostering good financial habits of your children early, specifically, the habits of budgeting and spending within their means. Talk to your teenage children about financial responsibility and the harm of abusing credit cards long before you allow them to have one.

If you are still not confident about your children’s ability to handle their personal finance, alternatively, during their freshman and sophomore years you can give them debit cards to use. That way, you can monitor their spending while teach them how to spend responsibly.

Another option of giving your

college students a chance of building their credit history is for parents to

add them as authorized users of parents’ credit cards. But, parents be aware,

you are ultimately responsible if your children rack up large credit card debt.

So parents need to think it through before adding your kids as authorized

users.

If your kids demonstrate financial responsibility during his or her freshman and sophomore years in college, then you can decide if they can apply for their own credit cards in junior or senior year.

One kind of credit cards students and parents may consider is so called secured credit cards. These cards can be ideal for college students who have no credit history or income. These cards are secured with a cash deposit, i.e. $300 or $500, from the card owner. Other than that, it works like a regular credit card. This kind of card is not a debit card. The cash deposit serves as a backup, not a payment for the card owner’s credit card bill. Students still need to pay their monthly credit card bill on time.

Ultimately, it is parents’ responsibility to know their children well and provide continuing guidance and supervision throughout their children’s college years in order for the kids to reap the benefits of building good credit history in college.