On September 18, 2024, the Federal Reserve announced that it cut its interest rate by half percentage point. The news quickly became financial headline worldwide.

So what is Fed’s interest rate? And why do Wall Street folks pay so much attention to it?

As United States’ central bank, Fed uses several tools for controlling the size and growth of the money supply. One of them is the Fed’s reserve requirement of its member banks. Member banks normally borrow from the Fed to increase their reserves to meet the Fed’s reserve requirements.

The rate that the Fed charges the member banks who borrow from the Fed is called “the discount rate.” Usually, most member banks would prefer to borrow funds from other banks rather than from the Fed. The interest rate member banks charge each other for borrowing is called the “federal funds rate.” This rate is usually slightly higher than the Fed’s discount rate and tends to change as the Fed’s discount rate changes.

Federal funds rate has been watched carefully as a guide to changes in other interest rates such as: bank deposit rate, mortgage rate, and auto loan, etc. It also has indirect impact on broader economy including employment, growth and inflation.

Whenever there is an increase or decrease in the federal discount rate there is a corresponding change in the federal funds rate. According to Fed, “the principal effect of an increase or decrease in the discount rate by the Fed is a corresponding change in the federal funds rate to the target level being sought by the Fed.” Hence, when we hear Fed Chairman talking about rate cut or rate increase, what he or she means is the Fed raising or lowering the target Fed funds rate range.

The current Fed’s federal funds rate target range is 4.75% – 5.00%, down by recent 0.5% cut.

Given its huge impact on financial markets worldwide, it’s not an overstatement by saying that the federal funds rate is one of the most important interest rates in the world.

Receiving a diagnosis of autism for your child can be overwhelming and emotional. However, it’s important to remember that early intervention and support can make a significant difference in your child’s development and quality of life. Here are some steps you can take after your child has been diagnosed with autism:

Learn About Autism

Autism is a complex neurodevelopmental disorder that affects social communication and behavior. There is a wide range of symptoms and severity, so it’s important to educate yourself about autism and how it may impact your child. Read books, articles, and blogs written by autism experts, attend support groups, and consult with your child’s healthcare provider to understand your child’s specific needs.

Create a Support Network

Having a support network can help you and your child navigate the challenges of autism. Reach out to family and friends for emotional support, and connect with other parents of children with autism through support groups or online communities. Consider hiring a therapist or counselor to help you and your family cope with the emotional stress of the diagnosis. If you are concerned about the cost of caring for a child with autism, a financial professional with expertise in special needs planning can help you sort out various options available to you to pay for the care your child needs.

Seek Early Intervention Services

Early intervention services are crucial for children with autism, as they can help improve their social, communication, and behavior skills. Contact your state’s early intervention program or your child’s healthcare provider to learn about available services in your area. These services may include speech therapy, occupational therapy, and behavioral therapy.

Create a Routine and Structure

Children with autism often thrive on routine and structure. Establish a consistent daily routine and schedule, and use visual aids, such as picture schedules or charts, to help your child understand and anticipate daily activities. Provide clear and consistent expectations, and use positive reinforcement to encourage good behavior.

Advocate for Your Child

As a parent, you are your child’s best advocate. Be involved in your child’s education and healthcare, and speak up if you feel your child’s needs are not being met. Stay informed about your child’s rights and legal protections, such as the Individuals with Disabilities Education Act (IDEA), and work with your child’s healthcare provider and school to ensure they receive appropriate accommodations and support.

Take Care of Yourself

Caring for a child with autism can be challenging and exhausting, so it’s important to prioritize self-care. Make time for activities that you enjoy, such as exercise, hobbies, or spending time with friends. Seek support from family and friends, and consider joining a support group for parents of children with autism.

Receiving a diagnosis of autism for your child can be overwhelming and emotional, but taking action early on can make a significant difference in your child’s development and quality of life. Remember that every child with autism is unique, and there is no one-size-fits-all approach to autism care. Work with your child’s healthcare provider and education team to develop a personalized plan that meets your child’s individual needs.

Financial planning is a pathway to independence and empowerment for women. Having control over one’s finances enables autonomy, the ability to make informed decisions, and a sense of security irrespective of life’s changes or unforeseen circumstances.

Historically, women have faced unique challenges in the financial realm, making strategic planning and preparation all the more crucial.

Challenges Women Facing Today

Longevity and Retirement

Women typically live longer than men, which means their retirement savings must stretch further. Yet, due to earning disparities and career breaks for care-giving roles, many women have smaller pensions or retirement funds. Therefore, robust financial planning becomes essential to ensure financial security during retirement years.

Career Interruptions and Flexibility

Women often encounter interruptions in their careers due to family obligations or care-giving responsibilities. These interruptions can impact income and savings, making it vital for women to plan and manage finances to navigate these transitions effectively. Creating financial strategies that accommodate career breaks and flexible work arrangements becomes imperative.

Healthcare Costs and Long-Term Care

Women generally have higher healthcare expenses, including longer life expectancies and potential long-term care needs. Financial planning must account for these factors, ensuring sufficient savings and insurance coverage to address healthcare costs effectively.

Steps Towards Financial Empowerment

1. Education and Awareness

Promoting financial literacy through education and workshops tailored for women can foster confidence and informed decision-making.

2. Long-Term Financial Planning

Developing comprehensive financial plans that account for diverse career trajectories, family dynamics, and potential life changes is key.

3. Support Networks and Resources

Encouraging supportive networks and access to financial expertise/resources can provide guidance and mentorship crucial for women navigating financial complexities.

4. Encouraging Investment

Promoting investment education and showcasing the benefits of long-term investment strategies can empower women to grow their wealth effectively.

Financial planning is not just a matter of numbers; it’s a catalyst for empowerment and independence, especially for women. And that is why financial planning holds particular significance for women in today’s world.

Small business owners face a unique set of financial challenges, from managing cash flow to dealing with taxes and regulations. While running a small business is rewarding, it can also be difficult to navigate the financial landscape. Here are five common financial mistakes that we’ve identified that small business owners often make plus our tips on how to avoid them:

Mixing Personal and Business Finances

One of the most common financial mistakes that small business owners make is mixing personal and business finances. This can lead to confusion, errors, and even legal problems. It’s important to keep your personal and business finances separate by opening a separate bank account for your business and using it only for business expenses.

Not Tracking Expenses

Another common mistake is not tracking expenses properly. It’s important to keep track of all your business expenses, no matter how small. This will help you to identify areas where you can cut costs and improve your profitability. Use accounting software or hire a bookkeeper to help you keep track of your expenses.

Failing to Plan for Taxes

Taxes can be a major headache for small business owners, especially if they don’t plan ahead. Make sure you are aware of all the taxes you need to pay, including federal and state income taxes, payroll taxes, and sales taxes. Set aside money each month to pay your taxes, and consider hiring a professional to help you navigate the complex tax code.

Ignoring Cash Flow

Cash flow is the lifeblood of any small business. It’s important to monitor your cash flow regularly and to have a plan in place to address any shortfalls. You can improve your cash flow by invoicing promptly, offering discounts for early payment, and negotiating better payment terms with your suppliers.

Failing to Plan for the Future

Finally, small business owners often fail to plan for the future for their business and/or for themselves. It’s important to have a long-term strategy in place for your business, including plans for growth, succession, and retirement. Make sure you have not only a solid business plan but also a financial plan that outlines your business and personal goals and how you plan to achieve them. Consider hiring a financial advisor to help you develop a comprehensive plan for your business and your family.

Running a small business is challenging, but avoiding these common financial mistakes can help you to achieve success. Keep your personal and business finances separate, track your expenses, plan for taxes, monitor your cash flow, and have a long-term strategy in place. By avoiding these mistakes and making smart financial decisions, you can build a strong and profitable small business.

As the new year unfolds, it’s an opportune time to reevaluate and revamp your financial strategies. Whether you’re aiming to build savings, invest wisely, or clear debts, at the beginning of the year a solid financial plan can set the stage for a prosperous future. Here are some practical steps to kick start your financial journey in 2024.

1. Reflect on the Past Year

Before diving into new financial goals, take a moment to reflect on the previous year. Analyze your spending habits, review your investments, and assess how well you adhered to your budget. Understanding where your money went and what financial choices worked or didn’t work for you will provide valuable insights for setting achievable goals in the coming year.

2. Set Clear and Attainable Goals

Establish specific and achievable financial objectives for 2024. Whether it’s saving for kids’ college education, paying off debts, better management for your personal and/or business cash flow, increasing retirement contributions, or starting a new investment venture, define your goals with clear timelines and measurable outcomes. This clarity will help you stay focused and motivated throughout the year.

3. Create or Update Your Budget

A budget serves as a roadmap for your financial journey. Take account of your 2024 income from all sources including your company stock options/employee stock purchase, and evaluate your expenses, and savings goals to create a realistic budget for the year ahead. Consider using budgeting apps or spreadsheets to track your spending and identify areas where you can cut back or reallocate funds toward your financial goals.

4. Prioritize Saving and Investing

Make saving a habit by automating contributions to your savings and investment accounts. Consider setting up automatic transfers from your paycheck to your savings or retirement accounts to ensure consistent progress toward your goals. Explore different investment options based on your risk tolerance and long-term objectives to make your money work for you.

5. Review and Optimize Your Investments

Take the time to review your investment portfolio. Assess the performance of your investments and consider rebalancing if necessary. Diversify your portfolio to spread risk and align it with your current financial goals and risk tolerance.

6. Tackle Debt Strategically

If you have outstanding debts, prioritize paying them off systematically. Consider using the snowball or avalanche method—paying off debts either from the smallest balance to the largest (snowball) or from the highest interest rate to the lowest (avalanche). Choose the method that suits your psychological and financial approach best.

7. Educate Yourself

Stay informed about financial matters. Whether it’s understanding investment strategies, learning about new savings options, or staying updated on tax implications, ongoing education is key to making informed financial decisions.

8. Review and Update Your Insurance Coverage

Ensure your insurance coverage—health, life, home, and auto—is adequate and up-to-date. Life changes and market fluctuations might require adjustments to your insurance policies to adequately protect yourself and your assets.

9. Seek Professional Advice

Consider consulting with a financial advisor or planner. Their expertise can provide personalized guidance, especially when navigating complex financial situations or planning for major life events.

10. Stay Committed and Flexible

Financial planning is an ongoing process. Stay committed to your goals, but remain flexible enough to adapt to unexpected changes or opportunities that may arise throughout the year.

Starting the year 2024 on the right financial footing involves a combination of diligence, planning, and adaptability. Remember, financial decisions you make today can have significant financial impact in the long run. By taking proactive steps and staying focused on your financial objectives, you can pave the way for a more secure and prosperous future.

What is special needs planning? Different people have different definitions. We believe the goal and purpose of special needs planning is to assure individuals with physical, cognitive, or developmental impairment a place in the community appropriate to their capabilities, resources, and their needs.

Developing a Comprehensive Plan

Special needs planning is not just about creating legal documents. It’s about developing a comprehensive plan that takes into account all aspects of the individual’s life, including healthcare, education, employment, housing, and social activities, etc. The plan should encompass four elements: the life, resource, financial and legal plans. The plan should be flexible and adaptable to changing circumstances and should involve the input and involvement of the individual with disabilities and their caregivers.

Understanding Government Benefits

Individuals with disabilities may be eligible for government benefits such as Supplemental Security Income (SSI) and Medicaid. These benefits provide financial assistance and healthcare coverage, but they also have strict income and asset limits. Special needs planning takes into account these limits and helps to ensure that the individual does not lose eligibility for these benefits.

Creating a Special Needs Trust

A special needs trust is a legal tool that can be used to protect assets and ensure that the individual with disabilities continues to receive government benefits. Assets placed in a special needs trust can be used to pay for expenses not covered by government benefits, such as education, transportation, and recreational activities.

Planning for Caregiver Support

Caregivers play a critical role in the lives of individuals with disabilities, providing emotional, physical, and financial support. Special needs planning should take into account the needs of caregivers, including financial support, respite care, and legal protections.

Special needs planning involves understanding government benefits, using legal tools such as a special needs trust, planning for caregiver support, and developing a comprehensive plan. Special needs planning can help to ensure that the individual with disabilities receives the care they need while preserving their eligibility for government benefits and protecting their assets. It’s important to work with professionals who specialize in special needs planning to create a plan that meets the individual’s specific needs and goals.

Sending your child to college is a major financial commitment for most families, and the costs can be staggering. According to the College Board, the average cost of tuition and fees at a private, four-year college is over $37,000 per year. However, with some smart planning and a few key strategies, it is possible to send your child to their dream college without going broke.

Start Saving Early

One of the best ways to prepare for college costs is to start saving early. Even small contributions to a college savings account can add up over time, thanks to the power of compound interest. Popular college savings options include 529 plans and Coverdell Education Savings Accounts (ESAs), both of which offer tax advantages for qualified education expenses.

It’s important to start saving as early as possible, ideally when your child is born or even before. However, it’s never too late to start saving, and even small contributions can make a big difference over time.

Consider Financial Aid

Financial aid can be a valuable resource for families looking to send their child to college without breaking the bank. Financial aid can come in the form of grants, scholarships, work-study programs, and student loans. Some financial aid is need-based, while other aid is merit-based, and there are many sources of financial aid available from government agencies, private organizations, and individual colleges and universities.

To maximize your chances of receiving financial aid, it’s important to fill out the Free Application for Federal Student Aid (FAFSA) as early as possible. The FAFSA is used to determine your eligibility for federal and state financial aid, as well as aid offered by individual colleges and universities.

Research College Costs

When it comes to college costs, not all schools are created equal. It’s important to research the costs of different colleges and universities to find the best fit for your budget. In addition to tuition and fees, you’ll want to consider the cost-of-living expenses, such as room and board, transportation, and books and supplies.

It’s also important to consider the potential return on investment of different colleges and majors. Some majors and schools have a higher earning potential than others, which can help to justify the higher costs of attending certain schools.

Consider Community College or Online Programs

Community colleges and online programs can be a cost-effective alternative to traditional four-year colleges and universities. Community colleges typically offer lower tuition rates and can provide a valuable opportunity for students to earn college credits while saving money. Online programs can also be a flexible and cost-effective way to earn a degree.

It’s important to note that not all degrees and majors are available through community colleges and online programs, and it’s important to consider the potential impact on future job prospects when choosing an alternative education option.

Negotiate Financial Aid Packages

Finally, it’s important to remember that financial aid packages are not set in stone. If you feel that a college or university is not offering enough financial aid, it’s possible to negotiate for a better package. This may involve appealing for more aid, asking for a re-evaluation of your financial need, or exploring other options such as work-study programs or external scholarships.

Sending your child to college is a major financial commitment, but with some smart planning and a few key strategies, it is possible to send your child to their dream college without going broke. By starting to save early, exploring financial aid options, researching college costs, considering alternative education options, and negotiating financial aid packages, parents can better prepare for the costs of higher education and help their children achieve their academic and career goals.

Achieving a net worth of one million dollars is a significant accomplishment that can offer financial security and peace of mind. However, it’s crucial to avoid making common financial mistakes that can jeopardize your wealth and hinder your long-term financial goals. Here are three financial mistakes to avoid with your first million dollars:

Overspending and Lifestyle Inflation

One of the most common mistakes people make when they come into money is overspending and inflating their lifestyle. When you suddenly have access to more money, it’s easy to get carried away with extravagant purchases and lavish experiences. However, overspending can quickly deplete your wealth, leaving you with little to invest or save for the future.

Instead, it’s essential to maintain your spending habits and avoid lifestyle inflation. This means living within your means and not increasing your expenses significantly, even though you now have more money. Focus on saving and investing your money for the long term instead of spending it on short-term pleasures.

Failing to Diversify Your Investments

Another mistake to avoid with your first million dollars is failing to diversify your investments. Putting all your eggs in one basket, such as investing solely in real estate or the stock market, can be risky, as it exposes you to significant losses if that investment performs poorly. It’s crucial to diversify your investments across different asset classes, such as stocks, bonds, and real estate.

By diversifying your investments, you can reduce your overall risk and maximize your returns. However, it’s important to remember that diversification doesn’t guarantee a profit or protect against losses. It’s essential to conduct thorough research and consult with a financial advisor to determine the best investment strategies for your financial goals and risk tolerance.

Not Planning for the Future

Just because you’ve hit your first million doesn’t mean you can stop planning for the future. In fact, it’s more important than ever to plan for the long-term. This includes setting goals for retirement, estate planning, and creating a legacy for your family.

To ensure that your wealth is protected and your future is secure, consider working with a financial advisor. They can help you create a comprehensive plan that takes into account your current financial situation and your long-term goals.

In conclusion, hitting your first million is an incredible achievement, but it’s important to avoid these common mistakes to ensure long-term financial success. By avoiding overspending, diversifying your investments, and planning for the future, you can continue to build wealth and secure your financial future.

As you might have heard in the news, last Friday, March 10, 2023, Silicon Valley Bank (SVB) has collapsed and was ordered by regulators to shut down its business. Part of the reasons that its collapse caused great concern is that it is the biggest bank failure since the 2008 Financial Crisis.

The failure of SVB is caused by a classic bank run. SVB had cash deposits of many startup companies. As bad news about SVB started spreading, a large number of these companies along with other depositors scrambled to pull their money out of the bank at the same time. This created a bank run that doomed SVB.

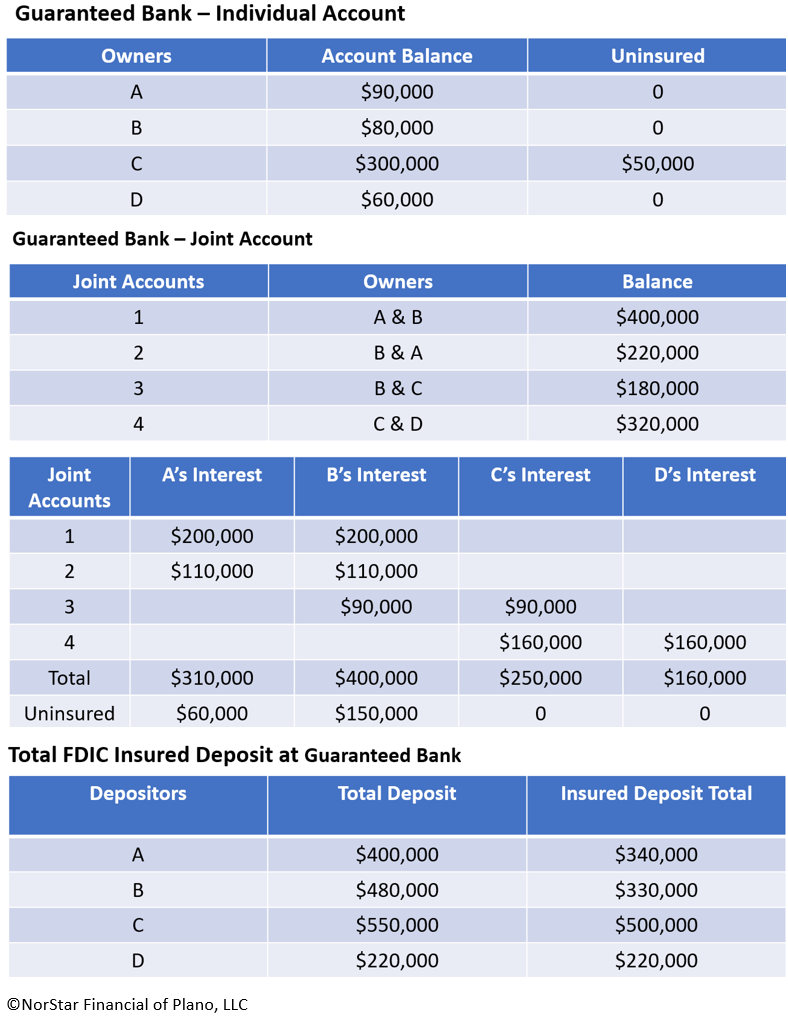

Naturally, you may wonder is my money safe in my bank?The Federal Deposit Insurance Corporation (FDIC) insures depositor accounts in banks and most types of nonbank thrift institutions up to $250,000. Deposits maintained in different categories of legal ownership, i.e. individual, joint account, irrevocable trust, and testamentary account are separately insured. As a result, a depositor can have more than $250,000 insurance coverage in a single institution. Here is how it works:

Likewise, the FDIC insures your deposits in each different institution in the same fashion as illustrated above. So, if you have $250,000 of deposit at each of four different banks, the FDIC insures a total of $1,000,000 of your deposits. As you can see, if you have a large sum of deposit exceeding $250,000, you need to either deposit the money into different types of accounts at the same bank, or spread the deposit among several banks.

Have you recently lost your job? Or changed job within the past 12 months?

If so, don’t let these events disrupt your life and personal finance. Here are some important financial issues that you need to consider now:

If you lost your job, do you have sufficient funds to last you until you land a new job?

Do you have emergency fund in savings account or money market fund to cover 6 months of your normal expenses? What other income sources are available to you? Also, don’t forget to set aside fund to cover your 2022 income tax liability.

If you changed job, has your income changed substantially?

If so, review and adjust your budget, tax projection and savings goals. Also, consider how the change in income will impact your ability to reach your previously set financial goals.

Do you have health insurance coverage?

If you changed job, are you covered by your new employer’s health insurance coverage? If not, coordinate insurance coverage so that there are no gaps in your health coverage.

If you lost a job, explore all health care options available to you. Depending on your current age, or the employment outlook, you may use your old employer’s COBRA for a short period of time to stay covered if you can find another job quickly or are eligible for Medicare soon.

Does your new employer offer Health Savings Account (HSA)?

If you have an HSA with your former employer, weigh the pros and cons of transferring the money in your old HSA into your new employer’s HSA.

Does your new employer offer Flexible Spending Account (FSA)?

If, before you changed job, you have contributed to your FSA with your former employer, you can still contribute to your new employer’s FSA as each FSA has its own annual limit.

Did you have employer sponsored life insurance and/or disability insurance?

If so, your employer sponsored life insurance and/or disability insurance will not follow you to your new job. You need to find out if your new employer offer employment related life and disability insurance, and whether the insurance benefits meet your needs.

Do you have a 401(k) plan with your former employer?

If so, you will need to decide whether to leave the money in the existing plan or roll them over. You need to weigh the pros and cons of both options.

Do you have stock options and/or deferred compensation arrangement with your former employer?

If so, review your stock option and/or deferred compensation plan documents to understand their vesting, exercising and distributing rules.

What’s next?

If you just got laid off, what your next step would be? It depends on your age and job skill sets. If you are a young professional, your next step might be looking for a new job or starting your own business. If you are an older professional you may be thinking about retirement or start a consulting business. Weigh your options and think them through.

If you are not sure you are making the right decisions, enlist a trusted financial professional to help you sort through your options. The financial decisions you make now could determine your financial destiny and affect the rest of your life.